Disaster Preparedness

Disaster claims process

What to expect when your home is damaged in a disaster

The hours following a disaster at your home will be stressful and heartbreaking. Dealing with your insurance claim — whether you are a homeowner or a renter — will be emotional, but should not be difficult. The National Association of Insurance Commissioners (NAIC) offers this overview of what you might expect and what you will need to file a claim after a disaster.

Immediately following the disaster

- To protect your property from further damage, you should make temporary repairs or arrange for a qualified professional to do so. Take photos of the damage and remove personal property if your home cannot be secured. Do not dispose of property until an insurance adjuster has reviewed it for your claim. Many policies include reimbursement for storage costs incurred until your home is repaired.

- If you can still live in the home, talk with your agent about critical repairs that need to be made. Whether you make the repairs or hire someone, save the receipts for your claim.

- If you need to find other lodging, keep records of expenses and all receipts. Homeowners and renter’s insurance generally provide limited coverage for expenses like meals, rent, utility installation and transportation.

Reporting your claim

- Most insurance companies have a time requirement for filing a claim. The process will go faster if you can locate a copy of your policy and home inventory.

- Call the company or visit a mobile claims center to start your claim. If you cannot find the company or agent’s number, call the Utah Insurance Department at 801-957-9200 or 800-439-3805 or use our Licensee Search opens in a new tab tool.

- You will be asked to list all items destroyed, damaged or missing. If you do not have a home inventory, begin making a list of items going room by room from memory. Include as much detail as possible, like where and when the item was purchased, the cost, brand name and model.

- If your car is damaged while in your garage/carport, it is covered by your automobile policy — not your homeowners policy. If you are insured by two separate companies for these coverages you must file a claim with both companies.

From your company

- Your insurance company will send an insurance adjuster to survey the damage at no cost to you. Public adjusters may offer the same services, but you would be responsible for any related fees. Check to be sure they are licensed with the Utah Insurance Department and ask for references and qualifications before retaining an independent adjuster.

- Do not feel rushed or pushed to agree on a settlement. If there are disagreements, try to resolve them with your insurer. If you cannot reach an agreement, the Utah Insurance Department can help you decide if arbitration or mediation is an option.

- Your full claim may come in multiple payments. The first will likely be an emergency advance and may include additional living expenses. The payment for your personal property and any additional living expenses will be made out to you. Payments for the structure may be payable to you and your lien holder if there is a mortgage on your home. Lenders may place that money in an escrow account to pay for repairs as the work is completed.

Making repairs

- Fraudsters often take advantage of the chaos following a disaster. When choosing a contractor to make repairs, check licensing and references before hiring. Always insist on a written estimate before repairs begin and do not sign any contracts before the adjuster has examined the damage. In some cases, the adjuster will want to see the estimate before you begin making repairs.

- Do not pay a contractor the full amount up front or sign over your insurance settlement payment. A contractor should expect to be paid a percentage when the contract is signed and the remainder when the work is completed.

- If the contractor finds hidden damage that was not discovered in the original assessment by the adjuster, contact your insurance company to resolve the difference. For any disagreements that cannot be resolved, contact the Utah Insurance Department about your recourse.

Additional information

- Flood and earthquake damage are not covered in a typical homeowners or renter’s policy. If you have a separate flood or earthquake policy, contact the company that wrote the additional policy to file your claim.

- If your insurance company delays in responding to your claim, call the claims department to find out if an adjuster has been assigned. Verify your contact details, especially if you have evacuated your home. Call the Utah Insurance Department if the delay is unreasonable.

- Even after settling your claim, if you think of items that were not in your initial loss list, contact your insurance company. Unless the company has paid the entire limit for the coverage of those types of items, it is possible the company will make an additional payment.

- If your damages exceed the amount of your coverage, federal agencies will occasionally provide grants or low-interest loans to assist with recovery following major disasters. Check with your local disaster center or Utah Insurance Department for more information.

After you have rebuilt

- Once you have re-established your home following the disaster, take time to do a home inventory. You can download a home inventory spreadsheet here opens in a new tab to help get started. You can also download the free NAIC myHOME Scr.APP.book app for iPhone opens in a new tab or Android opens in a new tab. The app guides you through capturing images, descriptions, bar codes and serial numbers, and storing them electronically for safekeeping. The app even creates a backup file for e-mail sharing.

- Once you have completed the home inventory, talk with your agent to make sure your homeowners or renter’s policy is adequate to cover your new investments.

Your home is your biggest asset

Do you have enough money in the bank to completely rebuild your home, pay off your mortgage, and replace all of your property? If not, keep reading.

What does my policy cover?

Just about every homeowner’s insurance policy covers fire, smoke, windstorms, lightning strikes, hail, explosions, vandalism, theft, and vehicle collision.

I don’t own a home so I don’t need to worry about it.

Unless you have the funds to replace everything you own, your belongings such as electronics, furniture, jewelry, and clothing need to be insured. Most apartments and landlords only have insurance to cover the actual dwelling; however, YOUR property is NOT typically covered by their policy. Most renters insurance policies offer protection for your belongings in case of power surges, water damage, fire, vandalism, and theft.

Great, I have a policy I am all set!

Not so fast, neither homeowners nor renters policies have coverage for floods or earthquakes.

Flood insurance

Why do I need flood coverage? I don’t live by water.

You don’t need to live near water to experience flooding. More than 70% of flooding in Utah in the past few years has been outside the state’s Special Flood Hazard area. Flooding caused by storms, melting snow, hurricanes, and water backup due to inadequate or overloaded drainage systems and broken water mains from outside the home are not covered by most homeowners and renters policies.

Don’t wait for the weatherman to tell you it’s time.

Buy flood insurance before a flood happens, otherwise you won’t be covered. Flood insurance policies typically take 30 days to go into effect. If you wait to purchase a policy until after a flood event threatens or occurs, your property won’t be protected from the damage caused by that flood event.

How do I purchase flood insurance?

The agent who helps you with your homeowners or renters insurance may also be able to help you with purchasing flood insurance. If your insurance agent doesn’t sell flood insurance, you can contact the NFIP Help Center at 877-336-2627.

For more information:

- Flood Insurance in Utah

- The National Flood Insurance Program (NFIP) opens in a new tab

- NFIP’s Flood Insurance Explainer Videos opens in a new tab

Earthquake insurance

What are the chances?

Earthquakes are impossible to predict and can cause major damage to your home and personal property. Earthquakes can occur at any time of year and any time of day. According to Earthquake Probabilities for the Wasatch Front Region in Utah, Idaho, and Wyoming there is a 43% chance of at least one large earthquake of magnitude 6.75 or greater occurring in the next 50 years. However, even small and moderate earthquakes can cause damage. About 500 earthquakes occur in the Wasatch Front region each year.

What does it cover?

Earthquake insurance covers repairs to your house, attached structures, your personal belongings, and additional living expenses. If you are a renter, you don’t need to worry about adding dwelling coverage.

What else do I need to know?

The deductible is an important consideration in earthquake insurance. It is a percentage of the dwelling coverage limit rather than a percentage of the amount of the loss. For example, a 5% deductible on a $100,000 policy would mean a deductible of $5,000 regardless of whether the loss was $20,000 or $100,000. In most cases, the base deductible is 5%, 10% or 20%. The deductibles are also unique in earthquake insurance because they apply to each coverage separately. For instance, if you have damage to your dwelling, damage to your personal property, and have loss of use, the deductible would apply separately for each of those three coverages. It is important to ask your insurer if they have one overall deductible or separate deductibles.

Don’t wait for tremors to start your policy!

For earthquake insurance, the waiting period is usually between 10 and 30 days. In addition, most insurers place a moratorium (a temporary suspension) on writing new earthquake coverage when there has been a recent earthquake in the area.

How do I purchase earthquake insurance?

To purchase earthquake insurance, you should start with your current homeowners or renters insurance agent. Earthquake insurance can be purchased as either a separate policy or an endorsement or rider to a traditional homeowner’s policy. If your current company does not write earthquake policies you may need to look to another company to purchase the policy.

For more information:

- Earthquake Probabilities for the Wasatch Front Region in Utah, Idaho, and Wyoming opens in a new tab

- NAIC/InsureU Earthquake Disaster Prep Guide opens in a new tab

So what do I do now?

- Take some time this week to review your policy.

- If you have questions or concerns, contact your local agent or your insurance company.

- Get the coverage you need and don’t wait until it is too late.

Earthquake insurance in Utah

Earthquakes send tremors of fear through most of us. Impossible to predict, earthquakes can cause major damage to your home and personal property, not to mention the loss of human life that can occur in severe earthquakes. Earthquake insurance is one way to protect one of your most valuable assets: your home.

Rating and underwriting

I. Actuarial Basis

There is more uncertainty attached to insuring against the peril of earthquake than almost any other peril addressed by property and casualty insurers. Less is known about the causes, locations, and magnitudes of earthquakes than other more predictable perils like fire. Primary factors that are considered and weighed when developing rates are the environment, historical results, building construction, etc.

II. Rating Territories

There are two approaches to earthquake rating. One divides the state into geological territories that generally follow the zones assigned by the U.S. Geological Survey. The second establishes one statewide rate. Individual company decisions to follow one method over the other are based on various factors unique to each company.

III. Deductibles

The deductible is an important consideration in earthquake insurance. It is a percentage of the amount of insurance, or limit of liability, rather than a percentage of the amount of the loss. For example, a 5% deductible on a $100,000 policy would mean a deductible of $5,000 regardless of whether the loss was $20,000 or $100,000. In most cases, the base deductible is 5%, 10% or 20%. Some insurers offer higher deductible percentages for a reduction in premium.

Another unique element of the earthquake deductible is that, in most cases, it applies to each coverage separately. For example, a 5% deductible on a $100,000 policy would be applied as follows (per the HO-3 standard homeowners coverage form):

| Coverage | Limit | Deductible |

|---|---|---|

| A – Dwelling | $100,000 | $5,000 |

| B – Other structures (10% of A) | $10,000 | $500 |

| C – Personal property (50% of A) | $50,000 | $2,500 |

| D – Loss of use (20% of A) | $20,000 | $1,000 |

One reason for the high deductible is that insurers cannot spread earthquake risks across the nation, or even across an individual state, as they spread fire and other property risks. This is because the exposure to earthquake is based on where an individual lives unlike the exposure to fire that can occur anywhere. As a result, only those who live in an area where the exposure for earthquake is high purchase it. This is also the reason for high premiums.

IV. Waiting Periods

Another unique element of earthquake insurance is that most insurers require a waiting period, usually from 10 to 30 days, before they will bind coverage for a new applicant. Furthermore, most insurers place a moratorium on writing new earthquake coverage when there has been a recent earthquake in the location in question. When there has been recent seismic activity, individuals rush to add earthquake coverage. After the panic dies down, they cancel the coverage. The exposure to risk and the expense to insurers are usually greater than the premium earned, so insurers choose not to bind coverage in this circumstance.

V. Premiums

Pricing for earthquake insurance varies from insurance company to insurance company. To arrive at the premium an insurance company will consider various factors, including the construction of the building, its location and the amount of coverage desired.

Coverages

Endorsements: In almost all cases, earthquake insurance is provided by means of an endorsement to a standard homeowners or business insurance policy. However, it can be provided as a stand-alone contract.

72 Hours: One element common to all coverage forms surveyed is the provision that one or more earthquake shocks that occur within a seventy-two hour period are considered to be a single earthquake. Aftershocks are common with earthquakes. This provision makes an earthquake and its aftershocks one occurrence. This prevents an insured being charged a separate deductible for each earthquake or aftershock.

Flood or Tidal Wave: Another common element is that coverage is excluded for flood or tidal wave of any nature, whether caused by, resulting from, contributed to, or aggravated by an earthquake.

Marketing

Though most insurers will provide earthquake insurance, few of them actively market the coverage. It is usually provided only at the request of the insured. You can find out who the top 20 companies are that market this coverage in Utah by going to our Earthquake Report found in the Market Share Reports.

Special programs for homeowners

In Utah, there are a couple of options other than endorsing a homeowners policy available to insureds. These policies are actually Difference in Conditions (DIC) policies. They provide catastrophe coverages not normally included in a basic homeowners policy and include earthquake and flood coverages. These programs are offered through many licensees.

As always it is important to understand the policy and coverage it affords. To do so you may want to review a sample policy prior to purchase.

For more information on Earthquake preparedness visit:

Flood insurance in Utah

Utah is a desert state, with low yearly rainfall amounts. As a result, flooding is not uppermost in the minds of most Utahns until it is too late.

Homeowners insurance does not cover losses due to flooding. Flood insurance policies are available through the National Flood Insurance Program (NFIP). If your agent does not write flood insurance you can find one using the links below:

- Floodsmart: https://www.floodsmart.gov/get-insured/flood-insurance-provider

- Utah Association of Independent Agents: https://www.utahia.org/default.aspx (or call 801-269-1200)

To see what is covered under the NFIP flood policy, visit https://www.floodsmart.gov/get-insured/buy-a-policy.

To get a list of 20 insurance companies selling flood insurance through NFIP or Private Flood Insurance in Utah, go to our Market Share Reports and look up the Flood Insurance report for the most recent year.

It’s a good idea to have the same agent who writes your homeowners or other insurance policies also write your flood insurance policy so in the event you need to file a claim, you only have to work with one insurance agency or company.

You can also get a quote directly from NFIP at https://www.floodsmart.gov/policy-quote/. Using some basic information about your property. After completing the quote, NFIP will help you find an agent to finalize your policy.

- Agency Producers: To be included in the NFIP policy quote tool, you must apply and be approved by FEMA. Information about the process is at https://agents.floodsmart.gov/agency-registry.

Be aware that flood insurance policies usually have a 30-day waiting period before they take effect, so the time to purchase is now.

Find out more about flood insurance at FEMA’s National Flood Insurance Program site.

To find out what flood zone you live in, and much, much more go to floodsmart.gov.

For help with an existing policy purchased directly from the NFIP, call 800-638-6620.

Special programs for homeowners

There are policies known as Difference in Conditions (DIC) policies. They provide catastrophe coverages not normally included in a basic homeowners policy and include earthquake and flood coverages. These programs are offered through many licensees.

As always it is important to understand the policy and coverage it affords. To do so you may want to review a sample policy prior to purchase.

Flood links

- Consumer Alert: Evaluate your need for flood insurance now

- Utah Communities Participating in the National Flood Program

- FEMA: For more information about being prepared for a flood.

- Flood Insurance 101: FEMA Region VIII Training

- Flood Map: Where are you on a flood map?

- How to Create a Home Inventory

- Insurance Companies Selling Flood Insurance in Utah & Other States

- Disaster Prep Guide — Flood

- Disaster Claims Process

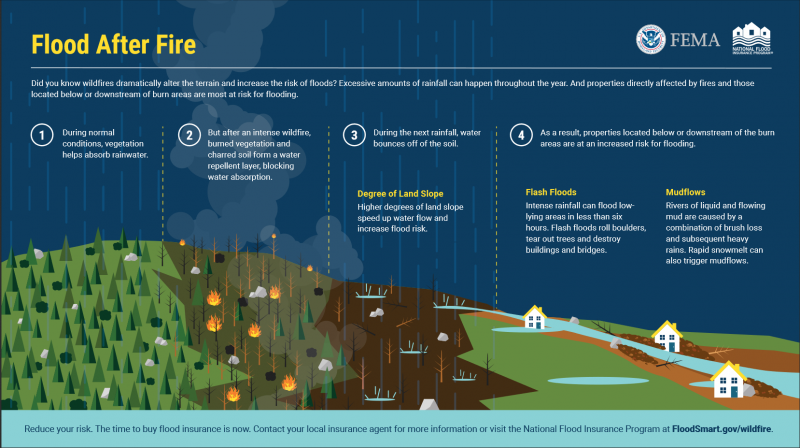

Flooding after a wildfire

When a wildfire burns vegetation in an area, it can take several years for the area to return to normal.

Vegetation, including grasses, bushes, and trees, all play a part in keeping the soil in one place. Roots push down into the dirt and spread out to keep the ground stable. Leaves and grasses also slow the flow of water, giving it more time to soak into the ground or evaporate.

When a fire burns that vegetation, there’s nothing to keep the ground in place or keep the water from rushing. Rains and snowmelt after a burn can easily turn into a flood or mudslide and can damage property in the days, months, and years after a fire.

Private insurance

Flood insurance can provide valuable peace of mind for people living downhill from a burnscar. It’s important to know your options and limits of the coverage you’re shopping for.

Most flood policies will cover the structure and contents of your home on the level that waters enter your home. If you live in a single-floor or multi-floor above-ground dwelling, that’s often enough.

If you have a home with a basement, you may be better off considering a difference in conditions policy. A difference in conditions policy offers combined coverage for events like flood, mudslides, earthquakes, and other similar perils.

Most flood policies have a 30-day wait period, which means that your policy becomes effective 30 days after you purchase it. It’s a good idea to reconsider your risk of flooding early every year.

Talk to your insurance agent about your flood coverage options. If you don’t have an agent, you can find one using our Licensee Search tool.

National Flood Insurance Program (NFIP)

The National Flood Insurance Program (NFIP) is run by the Federal Emergency Management Agency (FEMA) and is another way for Utahns to find insurance coverage.

Your insurance agent is also equipped to get you covered by an NFIP policy.

More information about NFIP flood insurance is available at https://www.floodsmart.gov/.

You can get additional information from the state’s floodplain manager at 801-538-3400 or https://floodhazards.utah.gov/ if you have questions.

What to do if you have windstorm damage

This is general information and suggestions. We recommend you review your insurance policy and discuss your situation with your insurance company for specific information.

- Take photos or video of your damage before cleaning up, removing trees and debris, or starting repairs.

- Mitigate your damages – Do what you can to protect your home and property from further damage, such as getting a temporary covering (blue tarp) on your roof to avoid the potential of water damage from any rain or snow storms coming our way.

- Keep all receipts – Temporary repair expenses are typically covered under the policy.

- Be safety minded – If you do plan to do temporary repairs yourself, please take adequate safety precautions.

- Landscaping damage – Damage to trees, shrubs, plants, etc., may not be covered from the windstorm.

- Removal of fallen trees

- Removal of the tree from the damaged property (home, shed, and garage) will probably be covered under your homeowner policy; however replacement of the tree will likely not be covered. This coverage may have a maximum dollar limit.

- Removal of fallen trees on your vehicle (auto, trailer, motor home, motorcycle, ATV) will probably not be covered under a homeowner or renter’s policy. The cost to remove a fallen tree from your vehicle may not be covered under any of your policies.

- When in doubt, check with your insurance company. It is best to discuss coverage with an adjuster – not with your agent.

- Check your policy deductible – Get an estimate before submitting the claim if you think your damage will be close to or under your deductible. You may not want to file a claim if the damage is not much more than your deductible.

- Using a contractor for temporary repairs and estimates

- Use only licensed and insured contractors.

- Contact the Utah Division of Professional Licensing (DOPL) to verify a contractor’s status.

- Request a certificate of insurance from the contractor.

- Keep in mind that there may be unlicensed individuals soliciting you to do the repairs.

- Report the claim

- Make the decision on whether or not you plan to submit your claim as soon as possible.

- The insurer will provide assistance to you through the claims process. They have years of experience handling insurance claims.

- It is best to discuss coverage with an adjuster – not with your agent.

- Some insurers have preferred pricing with contractors on their preferred list. Most have a list of contractors you may want to consider using.

- Many insurers are able to take your claim over the Internet.

- Our Licensee Search tool provides phone numbers for insurance companies, agents and agencies.

- Document everything – Document activity associated with damage to your property, keep track of time spent making temporary repairs. Keep a log of phone calls; date, time, name of the person you spoke with, call activity, etc.

- After the claim is filed

- The insurer has a minimum of 30 days to investigate your claim.

- Your insurance company should contact you within 15 days from when you filed your claim.

- Your insurance company should provide a substantive response to you within 15 days of a request from you.

If you encounter problems with your claim, contact your insurance company to discuss your concerns and give them the opportunity to resolve the matter with you. If you are not satisfied with the results, our consumer service personnel are available to help. Our help is free.

For questions contact the Utah Insurance Department’s Property and Casualty Division.

Wildfire in Utah

Utah's dry climate increases the risk of wildfires, which can quickly threaten homes and other property. Wildfires are a natural part of our ecosystem, but the expanding wildland-urban interface (WUI) and prolonged drought conditions have made the threat more serious. It's essential to be prepared and take steps to minimize the risk to your home and loved ones.

Protect your home:

Insurance is important in getting back to normal after a wildfire, but homeowners should take the following steps to protect their property and families:

- Create a Defensible Space: Clear brush, leaves, and flammable materials away from your home's perimeter. You should plan to clear about 100 feet around your home.

- Maintain Your Home: Keep roofs and gutters clean, seal gaps and cracks in your home's exterior, and use fire-resistant materials for landscaping.

- Prepare an Emergency Kit: Include essentials like water, food, first-aid supplies, important documents, and a battery-powered radio.

- Have an Evacuation Plan: Know your routes and designate a safe meeting place for your family.

The role of insurance

While prevention is key, insurance provides a vital safety net. Homeowners insurance can help you recover financially after a wildfire by covering:

- Dwelling: Rebuilding or repairing your home's structure.

- Personal Property: Replacing damaged or destroyed belongings.

- Additional Living Expenses: Paying for temporary housing and other costs while your home is uninhabitable.

Choose the right insurance

- Review Your Policy: Ensure you have adequate coverage for your home and its contents.

- Update Your Inventory: Regularly document your belongings to simplify the claims process in case of a loss.

- Shop Around: If your current insurer decides to no longer insure your home, look for a new one. The Utah market has many insurers that will take your business.

- Talk to Your Agent: Discuss your wildfire risk and any concerns you may have to ensure you have the right protection in place.

Don't wait until it's too late

Taking proactive steps now can make all the difference in protecting your home and belongings from the devastating impact of wildfires.

Wildfire Resources

The pages below are intended to help you plan for and get through a wildfire loss claim. View and download just the portions you need, or a complete wildfire packet.

- Before an Emergency: How to Prepare for a Wildfire

- During an Emergency: When You are Evacuated

- During an Emergency: After a Fire Loss

- Spotting Post-Disaster Scams: Protecting Yourself from Fraud

- Proving Your Loss: Navigating the Claim Process

- Claim Assistance & Support Resources

Wildfire links

Disclaimer – Links to Other Websites

As a convenience to our users, the Utah Insurance Department offers links to certain websites created and maintained by other public and/or private entities. The Department has no control over linked sites and cannot guarantee, or be held responsible for materials found on any non-departmental site. A link to another website is NOT a Department endorsement of that site.

Disclaimer – Use of Generative AI

Portions of this page were created using Google Gemini. All generated information was reviewed and improved by a human, and is accurate.